I. Introduction

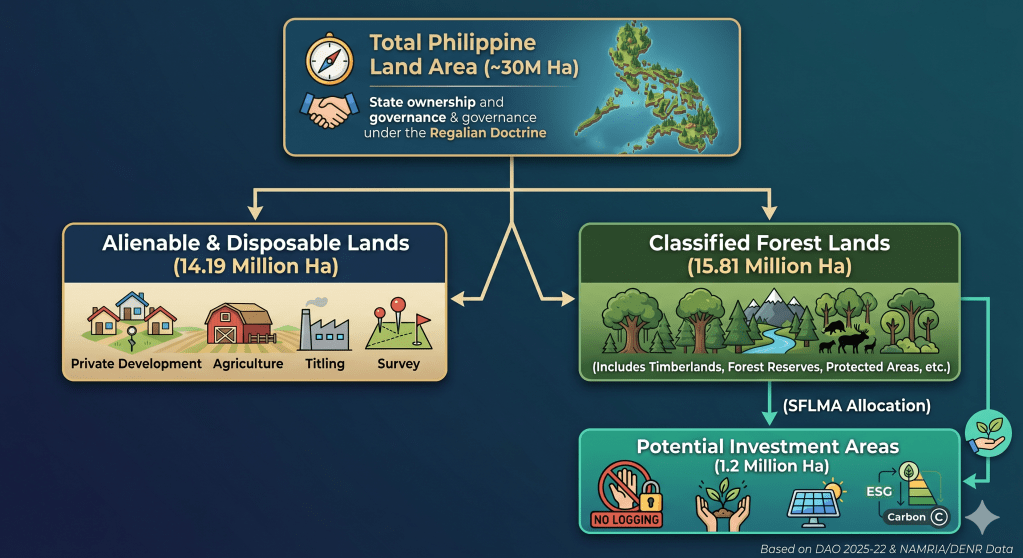

The implementation of the Sustainable Forest Land Management Agreement (SFLMA) under DENR Administrative Order No. 2025-22 marks a transformative shift from traditional, defensive forestry toward active environmental asset governance. This reform takes place against a complex legal backdrop where approximately 15.81 million hectares—over half of the Philippines’ total 30-million-hectare landmass—remain classified as public forest lands under the constitutional mandate of the Regalian Doctrine.

Historically, this system has suffered from institutional inertia, leaving official land boundaries largely unchanged since 2006 and creating a severe mismatch between legal designations and actual land use on the ground. However, the rise of the modern carbon economy has fundamentally reframed these spaces. Rather than treating forests merely as passive timber reserves or off-limits ecological zones, the SFLMA framework targets 1.2 million hectares of degraded public land—distributed across roughly 1,700 mapped parcels—to serve as climate infrastructure, carbon reservoirs, and natural capital assets.

Ultimately, this initiative places Philippine land governance at a critical intersection. The central challenge moving forward is balancing market-driven climate investments and carbon governance with the enduring constitutional principles of stewardship, social justice, and intergenerational responsibility.

II. The Carbon Economy and Legal Consolidation

One of the most consequential dimensions of the SFLMA is its architectural role in the emerging carbon economy. As international compliance and voluntary carbon markets mature, the framework provides the administrative and tenurial foundation required to host land-based carbon projects, verify forest carbon sequestration, and generate tradable carbon credits.

By offering long-term tenurial security, the SFLMA lowers the political and regulatory risk for institutional investors looking to fund nature-based solutions (NbS). Reforestation projects under this framework are uniquely positioned to serve as high-quality carbon sinks capable of issuing verified offsets for both domestic and international transfer.

Furthermore, this framework serves a critical state interest in regulatory streamlining. The SFLMA replaces and consolidates older, fragmented forest tenure systems, officially retiring:

- Industrial Forest Management Agreements (IFMA)

- Socialized Industrial Forest Management Agreements (SIFMA)

- Select commercial components of Community-Based Forest Management Agreements (CBFMA)

By collapsing these disparate instruments into a single governance mechanism, the DENR aims to eliminate conflicting land-use mandates, minimize institutional red tape, and lower transaction costs for clean-energy and conservation proponents. As the DENR noted during its rollout, the framework is explicitly designed to simultaneously generate rural employment, stimulate local economies, and boost the national gross domestic product (GDP) through sustainable forest enterprises.

III. Operationalizing SFLMA through the PENCAS Act

To properly realize its potential, the SFLMA framework must be linked directly to Republic Act No. 11995, otherwise known as the Philippine Ecosystem and Natural Capital Accounting System (PENCAS) Act. Passed to institutionalize the internationally accepted System of Environmental-Economic Accounting (SEEA), PENCAS provides the statutory framework that turns the theory of “environmental asset governance” into measurable fiscal and physical data.

┌────────────────────────────────────────────────────────┐│ R.A. 11995 (PENCAS Act) ││ National Macroeconomic & Data Standards │└───────────────────────────┬────────────────────────────┘ │ ▼ (Provides Baselines & Metrics)┌────────────────────────────────────────────────────────┐│ DENR DAO No. 2025-22 (SFLMA) ││ Project-Level Allocation & Concessions │└────────────────────────────────────────────────────────┘

1. The Data Engine for Asset Valuations

While the SFLMA identifies 1.2 million hectares of Potential Investment Areas (PIAs) for carbon sequestration and ecosystem services, establishing their baseline value without a standardized legal methodology invites speculation. The PENCAS Act solves this challenge by mandating the collection and compilation of official statistics on the depletion, degradation, and restoration of natural capital.

- Asset Accounts: Under PENCAS, the state must maintain strict physical and monetary accounts of timber and land assets, which directly inform SFLMA baseline data. This guarantees that carbon sequestration projects calculate genuine additionality rather than relying on unverified corporate metrics.

- Quantifying Ecosystem Services: PENCAS legalizes the valuation of “regulating services”—such as carbon storage, water filtration, and flood protection—giving SFLMA proponents a government-sanctioned data framework to back up ESG investments and carbon-credit accounting.

2. Macroeconomic Integration vs. Project-Level Finance

Under R.A. 11995, natural capital statistics are integrated directly into the country’s macroeconomic indicators, meaning major environmental accounts are co-released with traditional economic indicators like GDP. This creates a dual-layered governance system: PENCAS operates at the macro-level to track nature’s aggregated wealth, while the SFLMA operates at the micro-tenurial level. The SFLMA serves as the contractual vehicle allowing private and community actors to manage specific plots of land using the uniform accounting standards established under PENCAS.

3. Verification and Safeguards Against Greenwashing

One of the primary critiques of the SFLMA is the high risk of greenwashing and corporate regulatory capture. The PENCAS Act introduces a critical check on this through its institutionalized accounting metrics. If an SFLMA concessionaire causes ecosystem degradation or implements biodiversity-poor monoculture plantations under the guise of carbon offsets, the localized reduction in ecosystem asset accounts provides public interest litigants with actionable, government-backed data to support petitions for environmental remedies, such as a Writ of Kalikasan.

IV. Constitutional Boundaries: The Public Trust Intersection

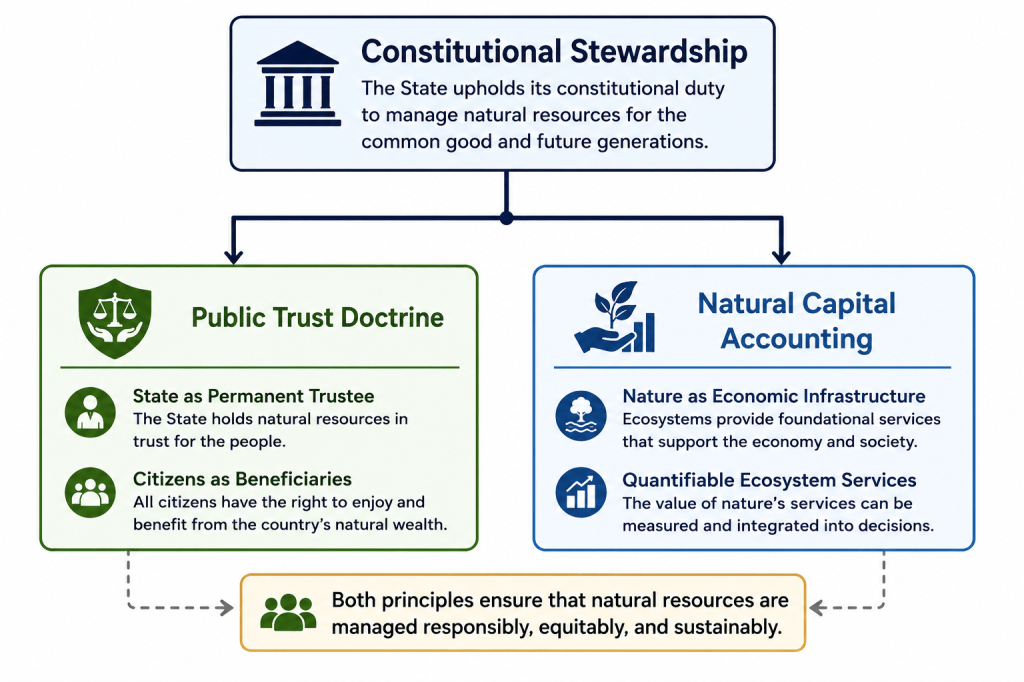

Despite its market-oriented mechanics, the SFLMA operates within rigid constitutional boundaries. Under Section 2, Article XII of the 1987 Philippine Constitution, all lands of the public domain and natural resources belong to the State under the Regalian Doctrine (Jura Regalia). Because public forest lands are inalienable, the SFLMA does not transfer ownership. Instead, it grants restricted stewardship and management rights, explicitly conditioned upon the continuous fulfillment of environmental obligations.

This arrangement operationalizes the constitutional philosophy that property bears a social function, meaning the right to utilize natural resources is inherently subordinated to the welfare of the common good. Consequently, the SFLMA sits at a complex legal intersection:

Under the Public Trust Doctrine, the State serves as the perpetual trustee of the nation’s natural wealth, while private and community actors function as temporary, fiduciary stewards. Every SFLMA project must therefore operate within legally defined ecological limits, ensuring that the exploitation of the asset does not impair the underlying public trust.

V. Systemic Risks, Drawbacks, and Structural Critiques

While structurally ambitious, the SFLMA framework exhibits several vulnerabilities, regulatory gaps, and socio-ecological risks that require rigorous mitigation.

1. The Commercialization of Ecospace and Greenwashing

By treating forests as natural capital, there is an immediate risk that environmental governance becomes subordinated to market incentives. If forests are valued primarily for their carbon credit yields and commercial ESG returns, biodiversity and deep ecological integrity may take a backseat.

This commercial focus invites structural greenwashing. Without robust, third-party verification protocols and data-driven carbon audit registries, corporate actors might exploit SFLMA concessions as cheap corporate branding vehicles. Weak state oversight could lead to speculative carbon banking, double-counting of offsets, and the generation of low-integrity carbon credits that fail to achieve genuine additionality.

2. Corporate Concession Dominance and Elite Capture

The framework permits large-scale corporate participation, allowing single entities to hold management rights over extensive tracts of land—in some instances up to 40,000 hectares. This high ceiling raises significant concerns regarding elite capture and land concentration. If large conglomerates dominate the competitive allocation of Potential Investment Areas (PIAs), smaller cooperatives, local civil society organizations, and marginalized upland communities may be priced out of the environmental asset market entirely.

3. Overlaps with Ancestral Domains and IP Exploitation

Spatial mapping data from the DENR indicates a critical geographic tension: approximately 85% of identified SFLMA parcels partially overlap with roughly 15% of ancestral domains occupied by Indigenous Cultural Communities (ICCs) and Indigenous Peoples (IPs).

While the law mandates compliance with the Free and Prior Informed Consent (FPIC) process under the Indigenous Peoples’ Rights Act (IPRA), there is a structural risk that this participation becomes merely transactional or symbolic. If indigenous communities lack equal bargaining power or sophisticated legal representation, they may find themselves excluded from meaningful benefit-sharing mechanisms and long-term project governance.

4. Ecological Conversion and Monoculture Risks

From an ecological standpoint, carbon-sequestration math often favors fast-growing, non-native commercial species over complex, slow-growing native silviculture. Policy research from the University of the Philippines warns that if regulatory safeguards are weak, the SFLMA could inadvertently incentivize the conversion of remaining natural secondary forests into simplified agroforestry or monoculture plantation systems, compromising local biodiversity and watershed resilience in the name of carbon maximization.

5. Regulatory Capture and Institutional Capacity Gaps

Simultaneously managing and auditing more than one million hectares of geographically dispersed forest lands demands an unprecedented level of technical, technological, and regulatory oversight. The DENR currently faces significant budgetary, staffing, and technological constraints. Without advanced remote sensing, real-time drone monitoring, and corruption-resistant auditing platforms, the SFLMA framework remains vulnerable to regulatory capture, illicit land conversions, and enforcement failures on the ground.

VI. Conclusion: Anchoring the Future Framework

The SFLMA brings a foundational tension in modern environmental law to the forefront: Should nature be governed primarily as an inviolable public trust, or as a quantifiable economic asset?

The doctrinal significance of DAO No. 2025-22 lies in its attempt to merge these two paradigms. It demonstrates that the Philippines is actively transitioning from a legacy of reactive environmental regulation to a proactive strategy of environmental asset governance.

The policy challenge moving forward is not whether the Philippines should participate in global climate finance or build domestic carbon markets; rather, it is whether these market mechanisms can remain firmly anchored to constitutional stewardship, social justice, and the principle of intergenerational responsibility (Oposa v. Factoran).

The ultimate success of Philippine carbon governance will depend on the state’s ability to develop a comprehensive legal framework that balances private economic utilization with robust public accountability, ensuring that all environmental assets are managed to serve the common good. The SFLMA has opened the door to market-based conservation; the onus is now on the state, civil society, and private sector to build the governance architecture required to walk through it responsibly.

Selected references and links:

- DENR Administrative Orders and press releases (look up DAO No. 2025‑22 on DENR website): https://denr.gov.ph (search for DAO 2025‑22 / SFLMA)

- DENR–Forest Management Bureau: https://fmb.denr.gov.ph

- National Commission on Indigenous Peoples (NCIP): https://ncip.gov.ph (for FPIC processes and ancestral domain maps)

- NAMRIA / PhilGIS (spatial data portals): https://www.namria.gov.ph, https://philgis.org

- Global Forest Watch (deforestation alerts, mapping): https://www.globalforestwatch.org

- Integrity Council for the Voluntary Carbon Market (ICVCM) and Core Carbon Principles: https://icvcm.org

- IPCC land-use and forestry guidance (for MRV methodologies): https://www.ipcc.ch

- Oposa v. Factoran, G.R. No. 101083 (1993) (Supreme Court jurisprudence on intergenerational responsibility and public trust): https://www.lawphil.net/judjuris/juri1993/mar/GR_101083_1993.html

- University of the Philippines forest restoration research (sample reference): search UP Los Baños / College of Forestry and Natural Resources publications on reforestation and monoculture risks.

- Forest Trends and Ecosystem Marketplace reports on voluntary carbon markets and nature-based solutions: https://www.forest-trends.org, https://www.ecosystemmarketplace.com

- Green Climate Fund and Global Environment Facility (finance windows for MRV and NbS projects): https://www.greenclimate.fund, https://www.thegef.org