By Augusto B. Agosto, JD, EnP, Economist, Consultant

When most people think of property valuation, they picture land, buildings, machinery, and infrastructure—tangible assets that can be easily inspected, measured, and compared in the marketplace. For water-dependent enterprises, however, a more fundamental question often arises: What is the value of the resource that makes the entire enterprise possible?

A water treatment plant without water has little utility; pipelines without water cannot generate revenue; and reservoirs without water are merely empty storage facilities. Yet, traditional valuation approaches often focus heavily on physical assets while giving limited attention to the underlying resource and the legal rights that govern access to it.

Recent professional engagements involving bulk water supply systems, utility infrastructure, and water-related enterprises prompted me to revisit a question that sits precisely at the intersection of law, economics, environmental planning, and valuation: Can the value of a water enterprise be fully explained by land and physical improvements alone? The answer is considerably more complex than conventional appraisal practice suggests.

Who Owns the Water?

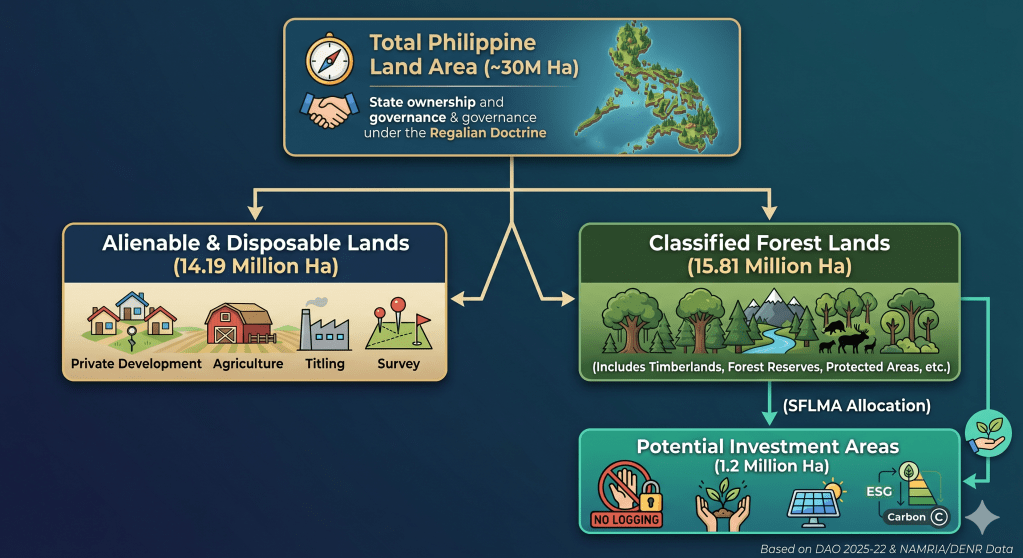

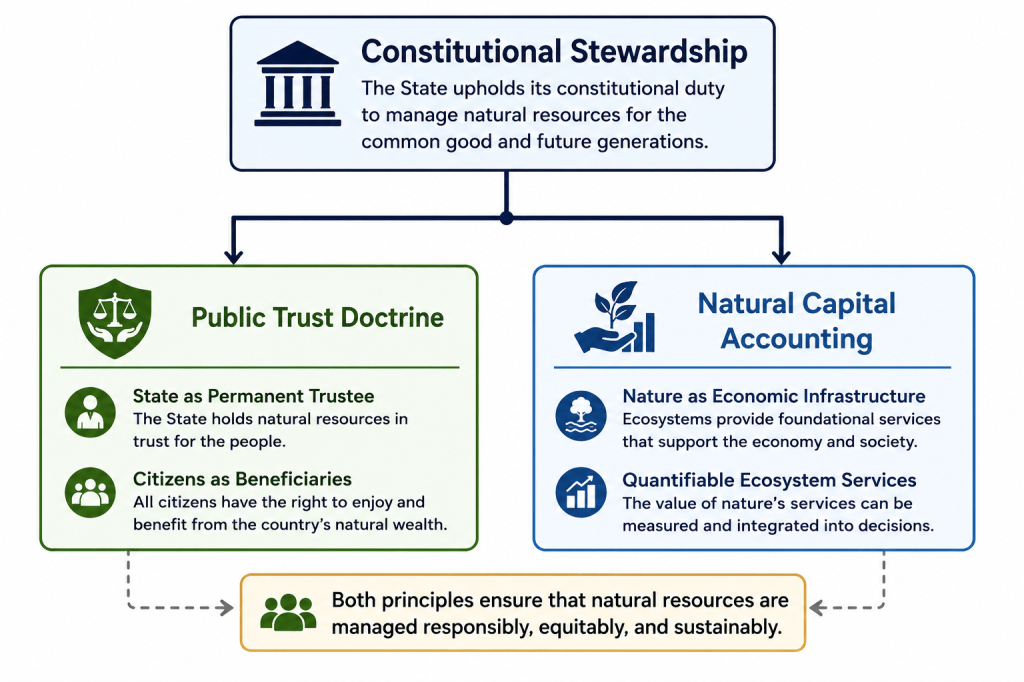

The starting point of any discussion on water rights in the Philippines is the Regalian Doctrine. Under Article XII, Section 2 of the Constitution, all natural resources—including waters—belong to the State. The Water Code of the Philippines (Presidential Decree No. 1067) further reinforces this by declaring that private entities may acquire only the right to appropriate and utilize water, subject to strict state regulation.

This distinction is critical for valuation professionals: private entities generally do not own the water itself. Instead, they acquire the legal authority to access, extract, treat, distribute, and utilize water for beneficial purposes. While a water permit is merely an administrative authorization from a legal perspective, from an economic perspective, that authorization represents a monumental source of value.

Water Rights as Economic Assets

Economics teaches us that value arises from scarcity. Although the Philippines is traditionally viewed as an island nation rich in water resources, many regions face acute water stress driven by population growth, rapid urbanization, watershed degradation, groundwater depletion, and climate-induced seasonal variability. As access to reliable water becomes premium, the economic significance of water rights increases proportionally.

Water rights act as economic catalysts by providing:

- Access to a Scarce Resource: Guaranteed entry into a restricted natural market.

- Security of Supply & Legal Certainty: Risk mitigation against operational disruptions and litigation.

- Priority of Use & Investment Opportunities: The baseline confidence required to deploy heavy capital for infrastructure development.

In effect, water rights serve as the operational bridge that converts unpriced natural resources into productive, revenue-generating economic assets.

Lessons from Practice: Beyond Tangible Assets

Several recent valuation assignments involving watershed-based bulk water supply systems and utility infrastructure projects forced a departure from standard real estate appraisal. These engagements required an evaluation that looked beyond physical infrastructure to assess raw water sources, regulatory authorizations, off-take contractual arrangements, and long-term hydrological sustainability.

One particular assignment involving a watershed-based bulk water supply system raised several non-traditional questions:

- What precise portion of enterprise value is truly attributable to land versus physical improvements?

- How should the raw, productive capacity of the surrounding watershed be quantified?

- What is the isolated economic value of the right to abstract and distribute water?

- How does the long-term reliability of the water source impact overall enterprise risk and value?

- To what extent do administrative permits and contractual off-take agreements contribute to the ongoing economic viability of the operation?

Answering these questions required moving past conventional property appraisal and venturing into resource economics, institutional rights, environmental planning, and natural capital accounting. The valuation ultimately demonstrated that the economic performance of the enterprise could not be explained solely by its tangible assets. A massive portion of its utility and income-generating capacity was inherently tied to the underlying water resource and the institutional frameworks safeguarding access to it.

Two Paths to Water Production

Observation of water enterprises in Cebu reveals an interesting operational dichotomy. Different enterprises produce marketable water through completely different asset profiles:

| Production Typology | Resource Reliance | Primary Value Driver |

| Natural Capital-Dependent | Watersheds, springs, and deep groundwater systems. | High reliance on natural replenishment and ecological health. |

| Technology-Dependent | Desalination plants and advanced treatment systems converting seawater or brackish water. | High reliance on produced capital, energy inputs, and technological investments. |

While both typologies generate revenue by delivering the same end product, their underlying asset structures differ fundamentally. One depends heavily on natural ecosystems; the other depends on engineered physical infrastructure. Yet, both share the same economic reality: without access to the baseline water resource (whether raw fresh water or raw seawater), neither infrastructure nor technology can generate revenue.

Natural Capital and Water Resources

The emerging field of natural capital accounting provides a precise framework for modernizing valuation practice. Natural capital refers to natural assets capable of generating flow-of-resource economic benefits. In this context, it encompasses:

- Watersheds, aquifers, and natural springs.

- Rivers, recharge areas, and critical forest ecosystems that regulate hydrological cycles.

Without healthy watersheds and functioning hydrological systems, physical water supply infrastructure loses its utility. Consequently, the comprehensive valuation of water enterprises demands that we look upstream at the sustainability and ecological health of the resource provider.

Beyond Valuation: Understanding How Water Creates Economic Value

The appraisal of water-dependent enterprises often begins as a valuation exercise. However, the analysis quickly extends beyond traditional questions of market value and into a broader examination of how value is created.

Water enterprises derive their economic significance not merely from land, infrastructure, or equipment, but from the interaction of natural resources, institutions, and markets. Watersheds generate water resources. Legal and regulatory systems allocate access through water rights and permits. Infrastructure transforms the resource into a usable product. Markets create demand. Together, these elements produce economic value.

Viewed from this perspective, water rights valuation is not simply an appraisal problem. It is fundamentally an economic inquiry into how natural capital is transformed into productive capital through institutional arrangements and investment.

The valuation question therefore becomes a gateway to a broader understanding of resource economics, natural capital, and economic development.

Recent developments—including the enactment of the Philippine Ecosystem and Natural Capital Accounting System (PENCAS), the Philippine Statistics Authority’s Water Accounts, and ongoing national water resource assessments—reflect a growing recognition that natural resources are not merely environmental assets but fundamental contributors to economic development and national wealth.

These initiatives have significantly advanced the measurement of water resources, ecosystem services, and natural capital. However, an important gap remains. Much of the existing literature focuses on water availability, water use, allocation, pricing, and conservation. Far less attention has been devoted to understanding how water resources create economic value and how institutional arrangements governing access to those resources influence investment, enterprise development, and wealth creation.

In particular, limited research has examined the role of water rights as institutional mechanisms that transform water resources into productive economic assets. The interaction between natural capital, legal entitlements, infrastructure investment, and economic production remains largely unexplored in the Philippine context. Understanding this relationship is increasingly important as water scarcity, climate risks, and competing resource demands place greater emphasis on the economic significance of water resources.

These questions form the foundation of the author’s ongoing research, which seeks to examine how scarcity, institutions, and water rights interact to create economic value within water-dependent enterprises and, more broadly, within the Philippine economy.

Conclusion

The discussion on water rights ultimately leads to a broader question than valuation itself. While appraisal seeks to measure value, economics seeks to understand how value is created. In the case of water-dependent enterprises, the answer extends beyond land, buildings, treatment facilities, and infrastructure.

The experience of examining bulk water systems suggests that economic value originates from the interaction of natural capital, institutions, and investment. Watersheds, aquifers, springs, and other water resources provide the physical foundation. The State, through the Regalian Doctrine and the Water Code, establishes the institutional framework governing access and allocation. Water rights and permits create certainty, enabling investment in infrastructure, treatment systems, and distribution networks that transform natural resources into economic output.

Viewed from this perspective, water rights are more than regulatory instruments. They serve as institutional mechanisms that connect natural capital to economic production. Understanding their role requires moving beyond traditional discussions of water use and toward a deeper examination of how water resources contribute to enterprise value, regional development, and national wealth.

Recent initiatives such as PENCAS, the PSA Water Accounts, and national water resource assessments signal a growing recognition of the economic importance of natural assets. Yet important questions remain. How do watersheds create economic value? How do institutions influence the allocation of scarce water resources? How do water rights support investment, productivity, and long-term development? These questions remain largely unexplored within Philippine literature and present opportunities for future research.

The inquiry that began as a valuation problem has therefore evolved into a broader economic question: how does a water resource become economic value? Exploring that question may not only improve valuation practice but also contribute to a deeper understanding of water governance, natural capital, and sustainable development in the Philippines. As water scarcity and climate-related challenges become increasingly significant, the ability to understand and account for the value created by water resources may prove essential to both economic policy and resource management in the decades ahead.