Bridging the gap between real estate, economics, and law.

Author: AB Agosto

A Juris Doctor and a Professor of Business & Economics at the University of San Carlos. Teaching finance, real estate management, and economics. He conducted lectures on valuation, environmetal planning and real estate in various places and occasions.

The impacts of Typhoon Tino offered a stark reminder. Floods are not solely natural hazards. Instead, they are hydrological imprints of spatial decisions. Land allocation, slope conversion, river encroachment, and watershed disruption manifest their consequences most visibly during extreme weather events.

The approval of Cebu City’s Comprehensive Land Use Plan (CLUP) 2023–2032 redirects the public agenda. It moves from legislative formality to the more consequential arena of implementation. The legitimacy of a land use plan is not proven by its passage. Instead, it is validated by the development outcomes it produces. This is especially true when these outcomes are tested by climate, geography, and population pressure.

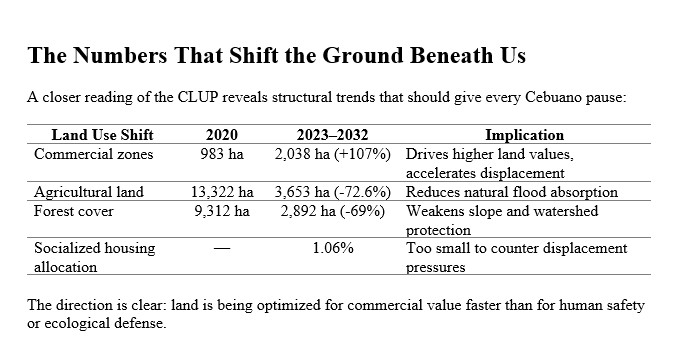

The new CLUP reveals major spatial shifts that carry long-term implications. Commercial land allocation more than doubled, while agricultural lands declined dramatically, and forest areas registered significant reduction. Meanwhile, socialized housing allocation remains strikingly minimal. The pattern points to a clear directional tilt. Commercial land expansion is accelerating faster than ecological buffering. It is also outpacing safe residential capacity.

As land values intensify within the urban core, households priced out of the city do not vanish. They relocate to the margins where land is cheaper and regulations are thinner. In Cebu, this relocation increasingly occurs toward upland barangays, steeper slopes, informal drainage basins, and unengineered terrain. The result is not accidental sprawl but policy-induced spatial displacement, where affordability gradients align dangerously with hazard gradients.

A persistent public misconception aggravates this risk calculus. Many people think that uplands newly classified under NIPAS (National Integrated Protected Areas System) are automatically protected. They believe these areas are free from settlement and land conversion. The law says otherwise. Under DENR Administrative Order 2008-26, Section 10(e), carried into theIRR of RA 11038, NIPAS areas may contain Multiple-Use Zones. In these zones, settlement, agriculture, agroforestry, extraction, and livelihood activities may be permitted. Even land tenure rights can be allowed, subject to the Protected Area Management Plan. In other words, NIPAS is a regulatory designation, not an automatic forest preservation guarantee. Hydrology responds to slope, soil porosity, and tree cover — not legal cartography.

Commerce expands more quickly than contour lines can withstand. Three outcomes converge. Land values rise without a parallel safe housing supply. Ecological buffers shrink faster than drainage systems are upgraded. Disaster risk is redistributed rather than reduced. The city becomes economically attractive yet environmentally fragile — bankable in dry months, breakable in wet ones.

The core policy question is therefore not “Should Cebu grow?” but rather, “Should Cebu grow without slope limits, drainage safeguards, housing balance, and hydrological discipline?” A land use plan that expands markets can be beneficial. However, if it creates flood risks for vulnerable communities, it does not represent a development strategy. It is a liability transfer encoded in zoning policy.

Urban planning must retire the outdated metric of success defined by hectares converted. It should adopt a new standard measured in households protected, watersheds stabilized, and risks prevented. Cities do not fail when the economy slows. They fail when slopes collapse and rivers overflow. Institutions run out of answers during the rainfall test they were meant to anticipate.

Cebu City now stands at a pivotal governance moment. The challenge ahead is not to stop development, but to civilize its direction. We need to build where water can be managed. Settling families in areas where slopes are stable is crucial. We must treat forests as infrastructure. Defending watersheds as life-support systems, not land reserves awaiting extraction, is vital.

The legacy of the CLUP will ultimately be judged by evacuation numbers. It will also be judged by flood marks and the geography of survival when the next typhoon arrives. Investment portfolios or skylines will not determine this legacy.

Progress is not proven by buildings standing in fair weather, but by communities still standing after the storm.

On October 26, 2025, the tailing pond of the URC Bais Distillery collapsed. As a result, thousands of cubic meters of molasses wastewater spilled into the Tañon Strait. This spill polluted over 3,000 hectares of marine waters between Negros Oriental and Cebu. The spill killed fish and discolored the water. It forced tourism operators in Bais and Manjuyod to suspend dolphin-watching and sandbar activities. What unfolded was more than an ecological crisis. It was an economic crisis as well. This crisis rippled through coastal communities. Their livelihoods depend on clean water, healthy fish stocks, and tourism income. Yet, despite the extent of the damage, there has been no official economic valuation. Without valuation, harm remains visible to the eye but invisible to the law.

Economic valuation is not about assigning a price to nature. It is about recognizing the real value of ecosystem services that sustain livelihoods and well-being. It transforms abstract losses into measurable, actionable data that policymakers and courts can use to demand accountability and rehabilitation. In the absence of valuation, justice often fails to materialize. The Clean Water Act requires the government to quantify and integrate environmental costs into planning and policy. The Philippine Ecosystem and Natural Capital Accounting System (PENCAS) Act also imposes this duty. However, in many cases these studies are never conducted. As a result, environmental disasters become administrative events instead of economic wrongs.

This failure is not theoretical. In the case of Ang Aroroy ay Alagaan, Inc. v. Filminera Resources Corp., environmental advocates in Masbate filed a petition. They aimed to stop gold mining operations. These operations were alleged to have caused water pollution and marine degradation. The case was dismissed. The petitioners did not provide scientific evidence linking the mining activity to the harm. They also failed to provide valuation evidence. The courts held that while the right to a balanced and healthful ecology is self-executory, it cannot rest on speculation. Without measurable data, there was no causal proof, and therefore no justice. This shows that when environmental damage is not quantified, the legal system has nothing to compensate. It has no foundation to impose liability. There is also no guide to direct restoration.

The law, however, provides a way to act amid scientific uncertainty through the precautionary principle. This principle is enshrined in Rule 20, Section 1 of the Rules of Procedure for Environmental Cases. It allows courts to act even when causation is not fully proven. It shifts the burden of proof to the polluter once a prima facie case of environmental risk is shown. In the landmark case Resident Marine Mammals of the Tañon Strait v. Reyes, the Supreme Court ruled that complete scientific certainty is unnecessary. Action should not be postponed if it can prevent environmental harm. In practice, however, the Filminera case demonstrates that courts hesitate to apply this principle. This happens when there is no baseline data or valuation study to demonstrate measurable harm. The absence of valuation deprives the precautionary principle of its factual footing.

In the URC Bais Distillery spill, the Environmental Management Bureau itself confirmed the contamination of thousands of hectares. They also confirmed the presence of fish kills and the closure of tourism activities. These are not speculative claims—they are facts. The prima facie case for environmental harm already exists. Therefore, failing to conduct an economic valuation at this stage runs counter to the very spirit of the precautionary principle. The principle demands preventive and remedial action even amid uncertainty, and valuation is the mechanism that gives it economic expression. Quantifying losses in fisheries, tourism, and household costs is necessary not just to demand accountability. Estimating non-market ecosystem values is also essential to guide rehabilitation and compensation.

When valuation is absent, the government cannot compute what justice demands. Victims receive no restitution, ecosystems receive no quantified restoration, and polluters face no cost proportional to the damage they cause. Without numbers, there are no remedies. Without valuation, there is no justice. And without accountability, pollution becomes merely another cost of doing business. The precautionary principle tells us to act before harm becomes irreversible. For that action to have meaning, it must be backed by measurement.

The Tañon Strait is not just a channel between two islands. It is a living system that feeds communities. It attracts tourism and anchors the regional economy. Its value is not speculative but measurable. Government agencies such as DENR, NEDA, BFAR, and local governments have a duty. They must translate this value into policy through formal economic valuation. Only then can we ensure that environmental protection is not symbolic but substantial. The spill in Bais should be a turning point. It should teach us that when damage has no price, accountability disappears. To value nature is to defend it. To measure loss is to make justice possible.

To value nature is not to commercialize it but to defend it. Measurement gives law and policy their moral weight. When damage has no price, accountability disappears. But when we count every lost fish, canceled tour, and poisoned tide, we remind the nation that ecology is economy. Justice begins with knowing what we have truly lost.

Thirty-six years since its 1989 ruling, Association of Small Landowners v. Secretary of Agrarian Reform remains the cornerstone of Philippine expropriation law—defining “just compensation” as the full and fair equivalent of property taken, not merely its cash price, and proving that reform and fairness can coexist under the rule of law.

It has been more than three decades since the Supreme Court decided Association of Small Landowners in the Philippines, Inc. v. Secretary of Agrarian Reform (G.R. Nos. 78742, 79310, 79744, 79777, July 14, 1989). Yet, the echoes of that landmark case still resonate across today’s debates on land rights, expropriation, and social justice. The case remains a constitutional compass for expropriation and land valuation. It guides the ongoing struggle to harmonize social justice with property rights.

This 1989 decision — penned by Justice Isagani A. Cruz — did more than uphold the constitutionality of agrarian reform under President Corazon Aquino. It defined how the State must pursue justice without committing injustice.

The 1989 decision, penned by Justice Isagani A. Cruz, arose at a pivotal moment. The Philippines had just ratified the 1987 Constitution. This called for genuine agrarian reform as a cornerstone of social justice. Acting under that mandate, President Corazon Aquino issued Proclamation No. 131 and Executive Order No. 229, launching the Comprehensive Agrarian Reform Program (CARP). These measures authorized the compulsory acquisition of private agricultural lands. Payment was provided not solely in cash. It also included government bonds, shares of stock, and other financial instruments.

Many landowners objected, arguing that such payment schemes were confiscatory and unconstitutional. They contended that agrarian reform could not override the constitutional protection of private property. They insisted that compensation must be paid in full and in money. The case reached the Supreme Court. The issue was not the legitimacy of reform itself. Instead, it was about the manner by which it was to be carried out.

Justice Cruz spoke for the Court. He upheld the constitutionality of the government’s agrarian reform measures. He delivered what would become one of the most defining interpretations of the Constitution’s takings clause. He explained that agrarian reform is “police power in purpose but eminent domain in method.” It is justified by the public welfare. Yet it involves the taking of private property. Therefore, it requires the payment of just compensation.

🟩 “The measure of compensation is the full and fair equivalent of the property taken from its owner by the expropriator. The word ‘just’ is used to intensify the meaning of the word ‘compensation,’ to convey the idea that the equivalent to be rendered for the property taken shall be real, substantial, full, and ample. Such payment need not always be made in money. It may be in other things of equivalent value, as long as it is real, substantial, and just.” — Justice Isagani A. Cruz, Association of Small Landowners (1989)

The Court emphasized that the question of just compensation is judicial in nature. Courts have the final word on what is fair and just, not any administrative or legislative body. This passage marked a turning point in Philippine constitutional law. It did not abandon market value as the measure of compensation. Instead, it broadened the understanding of how justice may be delivered in its equivalent form.

Justice Isagani Cruz, writing for the Court, clarified that the measure of compensation remains the property’s market value. This is the price that a willing buyer would pay to a willing seller under normal conditions. What the Court changed was not the measure, but the form.

The Court held that just compensation need not always be paid in cash. The owner must receive the full and fair equivalent of the property’s market value. This means that payment can be made through bonds, stocks, or other financial instruments, provided they reflect true, realizable worth.

The logic was both constitutional and practical. Implementing agrarian reform on a national scale would have been impossible. This task involves millions of hectares. It would not be feasible if the government were required to pay every landowner in full cash. The Court allowed flexibility. However, it insisted that the total value received must be real, substantial, and equivalent to what was taken.

In other words:

The market value remains the yardstick, while equivalent value is the means of payment.

The Court recognized that the price paid must reflect the full and fair value of the property taken. It should be the true market value. However, under exceptional circumstances, the government will pay through instruments of equivalent value. These instruments can be bonds or shares, as long as their worth is real and realizable. This doctrinal shift was both pragmatic and principled. The State can pursue a massive redistribution of land. It did so without collapsing under fiscal burden. Meanwhile, it safeguarded the constitutional rights of landowners to fair recompense.

Later decisions, including Land Bank of the Philippines v. Wycoco (2004) and Land Bank v. Honeycomb Farms (2009), reaffirmed this doctrine. Courts must determine just compensation based on market indicators, which include comparable sales, income potential, and zonal valuations. This holds even if the payment is made through other equivalent means. Thus, while the form of payment may vary, the standard of fairness does not. The Small Landowners decision preserved the essence of justice. It ensures that the value taken must be replaced by the same value returned. This must be done in whatever lawful form.

Beyond its technical rulings, the case represents a moral and constitutional reconciliation. It proved that reform need not be confiscation. Social justice must operate within the boundaries of the rule of law. The State may pursue redistribution and public welfare. However, it cannot deny fairness to those from whom the property is taken. In that balance lies the very heart of constitutional democracy.

More than three decades later, the decision continues to influence modern expropriation cases, such as Republic v. Arellano University (G.R. No. 260038, 2025), where the Court reaffirmed that just compensation cannot be based merely on administrative valuations or outdated schedules of market values. It must reflect all relevant market conditions. It should consider the property’s location and potential. Other factual considerations must make compensation truly fair. These modern cases, while dealing with urban development and public infrastructure, trace their constitutional lineage directly to Small Landowners.

The ruling’s wisdom resonates today in broader contexts. These include urban redevelopment, socialized housing, and environmental expropriations. It is also present in discussions on carbon markets and the just transition. Its enduring message is that reform must be fair, and fairness must be real. The law may adapt to new social challenges, but its foundation in justice and due process remains unchanged.

Association of Small Landowners remains a testament to the idea that progress and fairness are not adversaries but partners. The decision did not merely uphold agrarian reform; it humanized it. It emphasized that while the State may right historical wrongs, it must ensure the integrity of law is preserved. Thirty-six years later, it continues to serve as a reminder to both the government and citizens. Social justice should not be pursued at the expense of constitutional justice. No taking, however noble its purpose, is truly just without just compensation.

Why It Matters Today

The decision remains a bedrock precedent in property law, agrarian reform, and expropriation. It clarified the balance between individual property rights and collective welfare. This decision shapes how courts interpret “just compensation” in modern takings. These include cases from agrarian lands to urban redevelopment, road widening, and environmental expropriations.

In contemporary jurisprudence (e.g., City Government of Pasay v. Arellano University, 2025), the same principles continue to ensure that landowners are fairly compensated, while allowing the State to pursue inclusive, socially just development.

The Philippines is a nation blessed with incredible biodiversity. However, it is plagued by deforestation. The country is embarking on a new chapter in forest management. Environment Secretary Raphael P.M. Lotilla recently launched the Sustainable Forest Land Management Agreement (SFLMA). He hailed it as a “major shift.” It promises to revolutionize how the country’s 15.8 million hectares of forest land are managed.

On the surface, SFLMA sounds like a win-win. It streamlines seven fragmented forest tenure instruments into a single, renewable 25-year contract. It also encourages diverse uses like agroforestry, tourism, and conservation. The goal? Foster job creation, cut red tape, and promote inclusive economic growth. The DENR even rolled out complementary initiatives: “Forest for Life: 5 Million Trees by 2028” and mapping over 1.18 million hectares as “Potential Investment Areas (PIAs)” ready for private-sector cash.

Officials are calling it a “new era where conservation and commerce go hand-in-hand.” But is it truly a green revolution? Or does it hold hidden risks for the environment? What about the very communities dependent on these forests?

Legal and Economic Foundations: Operationalizing PNEACAS

The SFLMA is not merely a land-use policy; it is the operational execution of the Philippine National Ecosystem and Climate Accounting System (PENCAS) Law (Republic Act No. 11995). PENCAS legally mandates the integration of the environment’s economic value into national policy. It provides the foundational framework for the SFLMA’s valuation requirement. The agreement requires the calculation of the Total Economic Value (TEV) of the forest. It moves beyond traditional resource extraction models. This TEV approach is guided by the United Nations System of Environmental-Economic Accounting (SEEA) standards mandated by PNEACAS. It ensures that forest stewardship is financially incentivized.

The TEV calculation is divided into two distinct components, which define the roles of financial experts and environmental economists. The first, Valuation ofTangible Assets (Market Value), uses financial methods to evaluate profitability. These methods include Discounted Cash Flow (DCF) and Real Options Analysis (ROA). They determine commercial profitability from timber, non-timber products, and fixed user fees. This component is essential for attracting investment and securing financing.

The second and more innovative component is the Valuation of Intangible Services (Non-Market Value). This component monetizes public environmental goods, directly supporting the goals of PNEACAS. By converting ecological preservation into a quantifiable revenue stream, the SFLMA attempts to align conservation with long-term financial interest.

The Critical Role of the Economist

The economist’s function is to serve as the translator between ecological sustainability and financial viability. They achieve this by monetizing non-market benefits. This process directly addresses the core mandates of the PENCAS Law. They generate the data required for policy alignment and incentive design. Specifically, the economist calculates the value of carbon sequestration by applying the Social Cost of Carbon (SCC). This application turns stored carbon into tradable financial assets, known as carbon credits. This conversion establishes a critical revenue stream for reforestation. They apply the Replacement Cost Method to value watershed services. This method involves estimating the expense of building man-made infrastructure to replace the forest’s natural function. Furthermore, they use the Contingent Valuation Method (CVM) in surveys. These surveys quantify the public’s Willingness To Pay (WTP) for biodiversity. They also assess ecotourism. Through these processes, the economist ensures the SFLMA valuation is consistent with the SEEA framework. They guarantee the environmental statistics are credible and can be integrated into the national economic accounts. This demonstrates that the forest is worth more when preserved than when depleted.

Structural Incentives and Regulatory Risks

The SFLMA’s structural benefits include bureaucratic simplification. This reduces red tape. The 25-year long-term tenure provides the necessary security for substantial, sustainable investment. It mandates an integrated management plan, theoretically ensuring holistic management across production and protection uses.

However, critics cite significant policy risks. A primary concern is the potential for elite capture. This concern is driven by unequal land caps. These caps allow corporations to secure up to 40,000 hectares while capping People’s Organizations (POs) at 1,000 hectares. The technical complexity of TEV calculation adds an additional barrier. It requires sophisticated financial modeling such as DCF, ROA, and CVM. This complexity effectively excludes marginalized Indigenous Cultural Communities (ICCs) and POs that lack extensive external technical and financial support.

Furthermore, the policy faces criticism regarding its environmental oversight. The provision allows proponents to secure an Environmental Compliance Certificate (ECC) after the SFLMA is awarded. This reverses standard environmental procedure. It creates a potential loophole for environmentally damaging activities. The broad allowance for “special uses,” including industrial facilities, raises fears. There is concern about the industrial conversion of biodiverse areas into monoculture plantations or logistical hubs. This could potentially undermine the conservation goals inherent in the PNEACAS framework. The unresolved ambiguity surrounding the ownership of benefits from carbon credits also poses a risk. There may be disputes and unfair distribution of benefits among the state, investors, and local communities.

Safeguards and the Critical Path Forward

The DENR has attempted to mitigate these risks by articulating key safeguards. Key safeguards include the strict requirement for Free, Prior, and Informed Consent (FPIC) in ancestral domains. They also involve using Performance-Based Renewal. In this system, the 25-year contract renewal depends on stringent performance against specific Environmental, Social, and Governance (ESG) metrics. SFLMA holders are also mandated to include social development programs to ensure local employment and fair wages.

The success of the SFLMA hinges entirely on the rigorous enforcement of these social and environmental safeguards. For the policy to truly be a green revolution, it must overcome significant institutional challenges. It must ensure that the benefits quantified through the PNEACAS-mandated valuation framework are equitably shared. Community groups must be empowered to participate effectively. They should not be marginalized by the very system designed to value the resources they steward. Without this transparency, the SFLMA cannot succeed. Equitable implementation is essential. Despite its sophisticated economic design, it risks becoming a vehicle for resource consolidation and further environmental degradation.

The Supreme Court of the Philippines recently released a press statement. It is titled “SC: Just compensation in land expropriation must consider all relevant factors, not just market value.” This statement refers to its decision in G.R. No. 260038 (City Government of Pasay v. Arellano University).

The ruling reiterates a fundamental principle in expropriation law. Just compensation must be real, full, and fair. It is determined not by a single administrative figure, but through judicial evaluation of all circumstances surrounding the property.

However, the Court’s post also offers a chance to clarify a common terminological confusion. The use of “market value” as cited in the post does not refer to true open-market value. Instead, it refers to the Schedule of Market Values (SMV). Local assessors use this administrative instrument for taxation purposes.

Arellano University owned an 805-square-meter parcel of land in Barangay San Isidro, Pasay City. The City Government turned this property into a public road. It is now known as Menlo Street. This was done without expropriation proceedings or payment of just compensation.

The Pasay City Assessor’s Office had assigned the land a value of Php200 per square meter. This was based on its 1978 Schedule of Market Values. The trial court later used this figure to compute compensation.

The Supreme Court, however, clarified that such assessor-based valuations are not determinative of just compensation. They can guide fiscal assessments, but they are not substitutes for market evidence or judicial determination.

Market Value vs. Schedule of Market Values

This distinction lies at the heart of both valuation and constitutional law.

Concept

Meaning

Purpose

Authority

Market Value

The price a willing buyer would pay to a willing seller in an open market. Both parties act knowledgeably and without compulsion.

Reflects real market behavior, used in appraisals, investments, and expropriation.

Defined under PVS 102 and IVS 104; affirmed in Republic v. CA, G.R. No. 146587 (2002).

Schedule of Market Values (SMV)

A uniform benchmark value prepared by the local assessor for tax assessment purposes.

Ensures equity in real property taxation under the Local Government Code.

Authorized under Sections 212–216, LGC of 1991.

The PVS (Philippine Valuation Standards) and IVS (International Valuation Standards) define market value as:

The estimated amount as the price for which an asset exchanges between a willing buyer and a willing seller. This occurs in an arm’s-length transaction after proper marketing. The parties act knowledgeably, prudently, and without compulsion.

In contrast, the Schedule of Market Values is an administrative tool. It is updated every few years. It is designed to standardize taxation but not to represent real-time market dynamics.

The Supreme Court has consistently drawn this line in cases such as NPC v. Manubay Agro-Industrial Corp. and Republic v. CA: the SMV may be indicative. However, it cannot replace the judicial process of valuation. This process ensures constitutionally mandated just compensation.

My Letter to the Supreme Court

To support accurate public understanding of this distinction, I have respectfully written to the Supreme Court Public Information Office. My letter explains that the “Php 200 per square meter market value” is mentioned in the decision. It comes from the 1978 Schedule of Market Values. This should not be mistaken for actual market value as understood in valuation and jurisprudence.

In essence, my correspondence acknowledges the Court’s sound reasoning. It emphasizes the need to maintain terminological precision. This principle is crucial not only to valuation professionals but also to the legal system itself.

The phrase “market value” may appear technical. However, in matters of public taking, it defines the line between administrative convenience and constitutional fairness. When government takes private property, just compensation must reflect the property’s true worth—its economic value, not its tax-assessed figure.

Ensuring this distinction honors both the rule of law and the integrity of valuation practice. It safeguards landowners’ rights and guides courts, assessors, and appraisers toward a shared language of fairness and precision.

The City of Pasay v. Arellano University decision reinforces a timeless principle:

Just compensation is not a matter of administrative convenience—it is a constitutional right grounded in fairness and factual valuation.

As valuation professionals, we have a responsibility to ensure that public discourse around “market value” remains technically accurate. It must also be legally sound. Clarity in language leads to clarity in justice.

In today’s volatile property market, even fully leased buildings can face uncertainty when interest rates rise and yields compress. One of our clients is a developer with a 30-storey, 76-unit office tower in Bonifacio Global City. They sought clarity on whether their investment was still performing as expected. Through econometric analysis, we transformed complex market data into actions. This gave them financial insight that helped them see beyond occupancy rates. They focus on true value, risk, and return.

The Client’s Challenge

A private developer approached our team with a critical question:

“Is our 30-storey, 76-unit office building in Bonifacio Global City still financially viable under current market conditions?”

The client had completed construction two years earlier. The building was fully leased. They were concerned about rising interest rates. Modest rental escalations are eroding investment returns.

The property’s leasing structure appeared competitive. It includes a mix of bare-shell and fitted office units. These units range from PhP1,500 to PhP1,800 per sqm per month. However, management wanted to know if the building’s cash flows truly reflected its economic value. They questioned whether adjustments in pricing, escalation, or capital structure were necessary.

In short, the challenge was not occupancy — it was understanding profitability in a tightening capital market.

Our Approach

Instead of relying on conventional yield assumptions, our team applied econometric modeling. This is an analytical framework that links property-level performance to measurable macroeconomic drivers.

We began by reconstructing the building’s income statement. We also reconstructed rental schedules across 76 office units and all 30 floors. We factored in current lease terms and 3% annual escalations. Additionally, we used observed market data from Pinnacle Real Estate Consulting and Arcadis Philippines.

From there, we derived two distinct discount rates using both finance-based and property-specific risk models:

Method

Formula

Result

Finance-Based (CAPM)

R=Rf+β(ERP)+SRP

17.40%

Real Estate Build-Up

R=Rf+∑RiskPremiums

13.16%

Each parameter was anchored to empirical data. This includes the risk-free rate, beta, and risk premiums. These were tied to data from the Bangko Sentral ng Pilipinas, PSA inflation series, and Damodaran’s country risk tables.

By integrating these variables, we aligned the building’s valuation with economic reality rather than static, one-size-fits-all assumptions.

Findings: Translating Data into Decision

Our projection model covered a 10-year period, reflecting the economic life of the building’s interior improvements.

Discount Rate

Present Value of Cash Flows (PhP)

Fit-out & Equipment Cost (PhP)

NPV (PhP)

Interpretation

13.16%

11,801,358

12,472,358

–671,000

Breakeven (stabilized scenario)

17.40%

10,655,646

12,472,358

–1,816,000

Slightly negative (equity scenario)

Despite the modest NPV results, the cash inflows were sufficient to recover the capital outlay within the project’s economic life. This indicated a financially balanced asset — not speculative, but self-sustaining and capital-preserving.

The key insight for the client was that profitability was not being lost. It was simply redefined by changing macroeconomic conditions. In other words, the property’s yield had adjusted to reflect a maturing market.

We extended the analysis to examine how the project would perform under various economic shocks:

A 1% increase in the discount rate (e.g., due to rising interest rates) would reduce the property’s value by approximately PhP700,000.

A 1% increase in rental escalation would improve valuation by about PhP500,000.

This confirmed that interest-rate and capital-market movements have a greater effect on value than marginal rental adjustments.

The adopted PhP1,800 per sqm rate for fitted offices is advantageous. It places the property squarely within the prime BGC rental range of PhP1,400–PhP1,900. The effective yield is 7–8% per annum. This is a level consistent with institutional benchmarks in Metro Manila’s investment-grade office sector.

The results of the econometric analysis allowed the client to make well-informed and financially sound decisions. Our findings confirmed the current rental rate structure of PHP 1,500 to PHP 1,800 per square meter per month. This rate was aligned with prevailing market conditions. These rates match the conditions in Bonifacio Global City. Attempting to increase the rates further would risk higher tenant turnover without producing a proportional increase in building value. Hence, the most strategic course was to maintain existing rents, ensuring consistent occupancy and stable revenue streams.

Second, the study validated the client’s 3% annual escalation policy. It demonstrated that this policy accurately reflected the average inflation rate. It also matched the standard lease renewal adjustments in the area. This approach ensured that income growth would remain sustainable and competitive, balancing tenant affordability with long-term asset performance.

Finally, we advised the client to reclassify the building’s investment profile—from a short-term growth-driven asset to a core income property. This repositioning recognized that the building had already reached stabilization, with 100% occupancy and predictable cash inflows. The property could now serve as a capital preservation anchor within the client’s portfolio. It would provide reliable income to offset higher-risk, higher-yield developments elsewhere.

What initially seemed like a modest or even negative Net Present Value (NPV) was reinterpreted. It became a measure of financial efficiency. The building’s inflows matched its cost of capital. This indicated that it was performing exactly as expected in a mature market like BGC. Through this shift in perspective, the client gained a clearer understanding of the property’s value. The client also gained a more strategic framework for portfolio management, anchored in data, discipline, and economic logic.

This case highlights how econometric reasoning transforms real estate valuation from a static appraisal into a dynamic decision-making tool. We treated rents, yields, and escalation rates as variables linked to broader economic conditions. This approach helped us uncover not just the property’s value but also the logic behind it. The client learned that a neutral or breakeven NPV is not necessarily a weakness. It can signify equilibrium and maturity in a market. In this market, stability is the new form of strength.

For investors, the key takeaway is that macro-driven valuation brings clarity in times of uncertainty. Understanding how discount rates move with monetary policy provides a sharper sense of timing. Recognizing how escalation aligns with inflation sharpens your understanding of risk and opportunity. For developers, the lesson is strategic. Once a building reaches full occupancy and stable returns, it should be viewed as a core income asset. This asset anchors the portfolio and preserves capital rather than being seen as a speculative venture.

Ultimately, the study demonstrates that data and discipline lead to confidence. In Bonifacio Global City, every percentage point of yield and risk can mean millions in value. Econometric analysis offers a distinct advantage. It gives clients the ability to move beyond intuition. Consultants can also ground their investment strategies on measurable, defensible evidence.

By: AB Agosto, JD, REA, REB, REC, MA Economics (University of San Carlos) Paralegal – Real Estate, Environmental & Corporate Law

The Philippines, a nation of islands situated in the typhoon belt, remains one of the world’s most disaster-prone countries. The WorldRisk Report 2025 is a publication of Bündnis Entwicklung Hilft. It is also published by the Institute for International Law of Peace and Armed Conflict (IFHV) of Ruhr-University Bochum. It places the country among those with the highest global risk exposure. This conclusion is once again highlighted. The report has a special focus on floods. Floods are the most frequent and destructive natural hazard worldwide. Between 2000 and 2009, floods accounted for 44 percent of all global catastrophes, affecting more than 1.6 billion people and causing losses exceeding USD 650 billion. In the Philippines, flood vulnerability continues to rise because of climate-related rainfall intensification. Unregulated urbanization contributes to the risk. The degradation of natural buffers such as wetlands and mangroves exacerbates the situation.

These recurring flood events are no longer isolated environmental phenomena. They are now central to understanding how real estate functions. They are also central to understanding how real estate is valued. Climate risk directly influences property demand, development feasibility, and investment decisions. What once defined value purely in economic terms—location, accessibility, and market trends—now includes resilience, adaptability, and sustainability. Floods not only damage structures and displace communities but also recalibrate the long-term performance and desirability of land.

The Real Property Valuation and Assessment Reform Act (RA 12001), enacted in 2024, reflects this changing reality. It establishes a uniform national valuation framework, standardizes market-based approaches, and introduces mechanisms for adaptive reassessment. Among its provisions, Section 18 explicitly recognizes that disasters and calamities can alter property market values. It authorizes local government units to revise their Schedules of Market Values. This occurs whenever “significant changes” happen due to calamities or disasters. These changes can be man-made or natural. This provision marks a significant legal milestone. It integrates disaster risk into valuation governance. It acknowledges that climate events are legitimate economic variables. These variables can affect land and building worth.

This legal recognition aligns with the 2025 WorldRisk Report findings. The report calls for an integrated response. It combines four key perspectives: political, technological, social, and ecological. Political measures emphasize decentralized governance and the inclusion of risk management in land-use planning. Technological innovation encourages the use of satellite data, LiDAR mapping, and AI-based flood forecasting to inform planning and decision-making. Social resilience underscores community preparedness and traditional knowledge systems that reduce vulnerability. Ecological solutions advocate for mangrove reforestation, wetland restoration, and nature-based flood control, which simultaneously protect biodiversity and buffer human settlements.

In real estate valuation, these four dimensions translate into practical implications. Under the cost approach, flood exposure accelerates physical deterioration. It shortens the remaining economic life of improvements. Appraisers must apply higher depreciation rates. They also need to use more conservative estimates of useful life. The income approach must consider flood-induced operating expenses. It should also factor in reduced rentability and risk-based capitalization rates. These considerations help to account for uncertainty in income streams. Meanwhile, the market approach must segregate comparable sales based on hazard exposure. This is important since properties within flood-prone zones typically transact at discounted prices. These properties also exhibit longer marketing periods.

Beyond appraisal technique, the relationship between flood risk and property value also reflects broader behavioral and institutional adjustments. Developers now prioritize elevation, drainage systems, and green design. Lenders are requiring flood-risk assessments before approving mortgages. Insurers have introduced differentiated premiums based on hazard classification. These market adjustments demonstrate that resilience has become a form of economic capital—one that safeguards value and attracts investment.

Yet the transformation brought by the WorldRisk Report and RA 12001 extends far beyond valuation methodology. It is reshaping the Philippine real estate sector as a whole. Urban planning now integrates flood risk into Comprehensive Land Use Plans (CLUPs). Developers incorporate retention ponds and elevated designs as standard practice. Financial institutions are embedding environmental risk into credit assessments. The convergence of scientific data, legal frameworks, and market adaptation signals a new era in property governance. In this era, resilience is not peripheral but central to defining and protecting value.

In this evolving landscape, real estate valuation has likewise been methodologically reshaped. It is no longer a static appraisal of economic worth but a dynamic assessment of risk, sustainability, and adaptive capacity. Properties are now judged by their performance under pressure. This includes how they resist, how they recover, and how they remain useful during climate events. The very meaning of “value” has expanded: it now includes the ability to endure.

Ultimately, the 2025 WorldRisk Report and RA 12001 together redefine the fundamentals of real estate in the Philippines. The former provides the global scientific context for understanding hazard exposure. The latter establishes the national legal mechanism to respond to this exposure. Together, they transform how property is developed, managed, financed, and valued. In the age of climate uncertainty, the true measure of real estate is no longer limited to its square meters. It is also not defined by its location. Instead, it lies in its resilience per square meter.

In this century of rising tides and shifting ground, resilience is not just protection—it is value itself.

References

Bündnis Entwicklung Hilft & IFHV Ruhr-University Bochum. WorldRiskReport 2025. Available at: https://weltrisikobericht.de/worldriskreport/ Republic Act No. 12001. Real Property Valuation and Assessment Reform Act of 2024. Official Gazette of the Republic of the Philippines. Department of Finance – Bureau of Local Government Finance. Philippine Valuation Standards (PVS 2023).

When an earthquake caused the collapse of the Ruby Tower in Manila in 1968, the tragedy raised a profound legal question: could the contractors, architects, and engineers be held liable for damages, or was the destruction purely an act of God? This question was resolved in Nakpil & Sons v. Court of Appeals (G.R. No. L-47851, October 3, 1986), a case that remains a cornerstone of Philippine jurisprudence on real estate liability.

The petitioners argued that the earthquake was a fortuitous event, beyond human control, and that under Article 1174 of the Civil Code, they should be exempt from liability. The Court, however, examined the evidence and concluded that negligence in design and construction had contributed to the building’s collapse. The ruling made it clear: a fortuitous event does not excuse liability when human negligence concurs in producing the damage.

The Court declared, “The principle of fortuitous event cannot apply where the negligence of the obligor concurs with the fortuitous event in producing the damage. Negligence is not excused by fortuitous event.” In other words, while the earthquake was indeed an act of nature, the faulty workmanship and design defects were man-made, and together they caused the catastrophic failure.

This case remains directly relevant to real estate practice because it clarifies how responsibility is allocated when property is damaged by natural disasters. For builders and developers, Nakpil is a stern warning. It shows that compliance with the Building Code, zoning ordinances, and engineering standards is not optional but a legal duty. An earthquake may be unavoidable, but if poor materials, inadequate structural design, or shortcuts in construction contribute to the collapse, liability attaches. Developers cannot simply invoke force majeure; their reputation, financial exposure, and even criminal liability may be at stake.

For appraisers, the ruling highlights a subtle but crucial point. When valuing damaged property, it is necessary to ask: Was the loss caused solely by the disaster, or was it aggravated by negligence? If the latter, the cost to cure or diminution in value may be subject to claims against contractors, engineers, or insurers. This affects appraisal reports for insurance claims, litigation support, and even expropriation where consequential damages are assessed.

For insurers, Nakpil clarifies the boundaries of coverage. Many property policies exclude “acts of God” like earthquakes, but this case shows that where negligence coexists with a natural event, liability persists. Thus, insurers must carefully examine claims to determine if negligence by contractors or owners triggered coverage. It also guides insurers in drafting clearer clauses about fortuitous events, exclusions, and subrogation rights.

For property owners, the case is a lesson in vigilance and due diligence. Choosing competent contractors, hiring licensed engineers and architects, and ensuring that designs comply with earthquake-resistant standards are not just business decisions but safeguards against loss. Owners cannot assume that “insurance will pay” or that “the disaster was unavoidable.” The law demands that owners protect their property with foresight.

For the broader real estate industry, Nakpil underscores the link between law, valuation, and social responsibility. The safety and integrity of buildings directly affect communities, not just investors. When negligence meets disaster, lives and livelihoods are lost. By holding professionals accountable, the Supreme Court reinforced a culture of responsibility — one that appraisers, brokers, assessors, and developers must uphold in a disaster-prone country like the Philippines.

The continuing lesson of Nakpil is accountability- natural events may be unavoidable, but their impact is often determined by human foresight, planning, and diligence. In a country as disaster-prone as the Philippines, this doctrine safeguards the public by ensuring that responsibility cannot be avoided under the blanket excuse of force majeure.

Doctrine: Nakpil ensures that earthquakes and other disasters do not excuse negligence. Builders must build right, appraisers must distinguish causes of damage, insurers must test the limits of coverage, and property owners must demand quality. In real estate, accountability and preparedness remain the first defenses against natural calamities.

Further Reading

Full text of Nakpil & Sons v. Court of Appeals on Lawphil.net

Civil Code of the Philippines, Title I, Chapter 2 (Obligations and Contracts)

The ARROW Act (RA 12289) promises faster infrastructure and fairer compensation for landowners — but will it curb corruption or create new risks? Learn what appraisers and property owners must know.

Massive infrastructure projects in the Philippines often carry a double meaning. On one hand, they symbolize progress — roads that connect markets, airports that open trade, and power lines that electrify communities. On the other, they are dogged by delays, undervaluation of property, and allegations of corruption in right-of-way (ROW) spending. For property owners, expropriation has too often meant dispossession without fair payment. For taxpayers, billions intended for development sometimes disappear into inefficiency or worse, into private pockets.

The Accelerated and Reformed Right-of-Way (ARROW) Act (RA 12289) was passed to address these longstanding problems. It is framed as both accelerated — ensuring faster delivery of projects through calibrated deposits, ex parte writs of possession, and anti-delay rules — and reformed — standardizing valuations, expanding compensation, and mandating transparency. In theory, the law promises to close the loopholes that have long made ROW a breeding ground for corruption.

What Appraisers Must Know

For appraisers, the Accelerated and Reformed Right-of-Way (ARROW) Act (RA 12289) raises the bar of professional responsibility in ways that cannot be overstated. Under this law, the appraisal report is no longer just a supporting document — it is the linchpin of fairness in the determination of just compensation.

Valuation now begins with the Schedules of Market Values (SMVs) prepared by local government units under RA 12001, the Real Property Valuation and Assessment Reform Act. These SMVs are intended to provide an updated, standardized baseline to reduce arbitrary valuations. In the absence of updated SMVs, zonal values from the Bureau of Internal Revenue or assessed values may be used. However, these figures are only starting points. The law explicitly requires courts to weigh comparable sales data, sworn valuations by property owners, and independent appraisal reports. This keeps professional appraisers at the very center of the process: their expertise bridges the gap between mass appraisal (which may lag behind the market) and the constitutional requirement of “just compensation,” which demands property-specific fairness.

Beyond land valuation, the ARROW Act recognizes the full range of compensable interests that appraisers must document and value. Improvements, machinery, and structures must be valued at 100% of their replacement cost, subject to depreciation when determining deposits but fully recognized in final compensation. Crops and trees must be valued at market rates based on species, maturity, and productive potential. Partial takings — where only part of a parcel is acquired — require an assessment of the diminution in value of the remaining property, a task that often calls for a before-and-after analysis. The law also expressly allows for subsurface rights acquisition (for tunnels, pipelines, and conduits), which appraisers must value as easements or partial restrictions rather than outright takings.

This broadened scope makes appraisal practice more demanding but also more consequential. Appraisers must now master not only the sales comparison and cost approaches, but also agricultural valuation, easement analysis, and diminution-in-value methodologies. They must be familiar with engineering cost indices, Department of Agriculture commodity pricing, and even geotechnical impacts in subsurface cases. Every omission or weak assumption in a report may directly affect landowners’ rights and project budgets — or worse, provide room for undervaluation schemes.

What Landowners Must Know

For landowners, the Accelerated and Reformed Right-of-Way (ARROW) Act (RA 12289) is both a protection and a challenge. On the one hand, it expands what counts as compensable property. On the other, it requires vigilance to make sure rights are not overlooked or eroded.

The law broadens the scope of compensation significantly. Landowners are no longer limited to being paid for the bare land alone. They are entitled to just compensation that covers the value of the land, the 100% replacement cost of improvements and machinery, the fair market value of crops and trees, and even the diminution in value of partially affected parcels. This is critical because many families rely not only on their land but also on the homes, shops, or farms built upon it. Under RA 12289, these are recognized as integral to livelihood and must be paid for.

Importantly, the law also protects those who do not yet have formal titles. Long-time possessors of untitled land can still be compensated, provided they can present evidence such as tax declarations, DENR certifications declaring the land alienable and disposable, survey plans, and affidavits from disinterested persons or barangay officials. This closes a long-standing gap where informal but legitimate claimants were previously left without remedies.

However, landowners must also recognize the practical limits built into the law. Initial deposits made by the government when filing for expropriation are deliberately modest: only 15% of the land’s market value, but 100% of the replacement cost of improvements and 15% of crops. While this ensures that owners with houses, factories, or crops receive upfront money, those whose property is land-heavy but improvement-light may feel underpaid at the start. The balance is determined later by the courts as final just compensation, but this process takes time, and owners must be prepared for the cash flow gap.

The law also introduces a two-year freeze rule. Once a notice of taking is issued, any improvements added to the property may not be recognized for compensation. This rule is meant to discourage speculative or last-minute construction intended to inflate claims. For landowners, this is a warning: avoid sinking new investments into a property already tagged for acquisition, as they will not be reimbursed.

Promise or Risk?

Here lies the central tension of the Accelerated and Reformed Right-of-Way (ARROW) Act (RA 12289). The law is carefully crafted to accelerate infrastructure delivery while at the same time protecting landowners. By anchoring valuations to Schedules of Market Values (SMVs), it seeks to bring predictability to a process that used to be haphazard. By mandating public disclosure of right-of-way transactions, it holds agencies accountable in ways that past laws never did. By imposing sanctions on officials or private entities who delay or manipulate acquisition, it promises to bring discipline to a sector notorious for inefficiency and abuse. On paper, these reforms appear to strike the balance between speed and fairness.

But every promise also carries its shadow. SMVs, while standardized, remain products of mass appraisal. If they are outdated, they can undervalue land and deprive owners of just compensation. If manipulated at the local level, they can be skewed to benefit certain political or commercial interests. The ex parte writ of possession, designed to give the State quick access to property, is a powerful tool — but it can weaken a landowner’s leverage if the final fixing of just compensation drags on. Transparency requirements are strong in theory, but history has shown that agencies often find ways to delay, obscure, or underpublish the data the public needs to verify compliance.

The ARROW Act, then, stands at a crossroads. If implemented with integrity, it could finally provide a solution that curbs corruption, ensures fair compensation, and restores trust in public projects. But if captured by vested interests, it could just as easily become another source of corruption — with mass appraisal abused to justify lowball offers, safeguards ignored in practice, and speed used as a cover for unfairness.

The outcome depends not only on the text of the law but on the people who live under it. For appraisers, professionalism, independence, and defensibility are now essential, because their reports are the first line of defense against undervaluation and collusion. For landowners, preparation and vigilance are key — they must safeguard documents, assert their rights in negotiations, and demand the transparency that the law promises. For institutions, the challenge is consistent enforcement: ensuring that timelines are met, disclosures are made, sanctions are imposed, and that the balance between public need and private rights is respected.

In the end, the ARROW Act is not just a piece of legislation but a test of political will and civic vigilance. It challenges the Philippines to prove that it can build fast without breaking trust, that progress does not have to come at the expense of justice, and that corruption does not have to be the inevitable cost of development. Whether it fulfills its promise or slips into risk will depend on how well all actors play their part in the years ahead.

One of the landmark reforms in the Philippine criminal justice system is Republic Act No. 6981, otherwise known as the Witness Protection, Security and Benefit Act. The law was enacted to encourage witnesses to testify in criminal cases by granting them immunity from prosecution and providing protection and benefits that ensure their safety and livelihood. At the heart of this reform is the central role of the Department of Justice (DOJ), whose authority was tested in the high-profile case of Webb v. De Leon (G.R. Nos. 121234, 121245, 121297, August 23, 1995).

Under Section 12 of R.A. 6981, the DOJ has the power to admit witnesses into the program. Once admitted, the certification issued by the DOJ must be given full faith and credit by public prosecutors. This means that prosecutors are barred from including the admitted witness in any criminal complaint or information, and if the witness has already been charged, the prosecutor is duty-bound to move for his or her discharge. Admission also grants the witness immunity from prosecution for the related offenses, together with access to rights and benefits such as security, relocation, subsistence, and employment assistance.

This provision was challenged by petitioner Hubert Webb, who argued that only the courts, under Rule 119 of the Rules of Court, have the authority to discharge an accused as a state witness. He claimed that allowing the DOJ to decide on the admission of witnesses intrudes upon judicial prerogatives and violates the separation of powers.

The Supreme Court disagreed. It held that the prosecution of crimes is fundamentally an executive function, anchored on the constitutional duty of the executive branch to “faithfully execute the laws.” The discretion to determine whether, what, and whom to charge—including who may be used as a state witness—properly belongs to the DOJ as part of its prosecutorial power. The Court clarified that while Rule 119 empowers courts to discharge an accused once jurisdiction has been acquired, this authority is jurisdictional rather than inherent. It ensures that proceedings remain orderly, but it does not strip the DOJ of its primary role in deciding witness admissions under R.A. 6981.

The decision underscores the delicate balance between the branches of government: the executive determines who to prosecute and who to use as a state witness, while the judiciary supervises proceedings once a case is filed. By upholding the DOJ’s role, the Court strengthened the Witness Protection Program as a vital tool for combating crime. As the DOJ itself pointed out, many cases in the past had been dismissed due to witnesses refusing to testify out of fear or economic dislocation. R.A. 6981 and its interpretation in Webb directly address this challenge by protecting witnesses and ensuring their cooperation.

The Webb v. De Leon ruling affirms that the DOJ’s role in the Witness Protection Program is constitutionally sound and crucial for the administration of criminal justice. By empowering the DOJ to certify and immunize state witnesses, the law tackles one of the biggest obstacles in criminal prosecutions: the silence of those who know the truth. In a justice system often hampered by fear and intimidation, the law sends a clear message—witnesses will be protected, and their courage will not be in vain.